содержание .. 6 7 8 9 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2017 рік) - 8

OUR PERFORMANCE

ANNUAL REPORT 2017

117

116

system allocated to the transit

business is almost equal to

the value of pipelines used for

existing transit routes (currently

only Druzhba oil pipeline), which

comprises about half of total

value of oil transmission system as

of 31.12.2017.

If historical transit routes were

preserved (such as Samara –

Lysychansk – Tykhoretsk and

Brody–Yuzhny in reverse mode),

ROIC of oil transit would be much

lower.

If ROIC for the whole business

group of oil transit and

transmission is calculated for

2017, it would be 6%, which is less

than the appraiser’s cost of capital

(17.4%).

Oil domestic transmission:

UAH-denominated ROIC vs

cost of capital, %

2016

2017

–6�8%

–6�3%

17�4%

17�4%

ROIC

Cost of capital

Oil transit: UAH-denominated

ROIC vs cost of capital, %

2016

2017

20�5%

19�9%

17�4%

17�4%

ROIC

Cost of capital

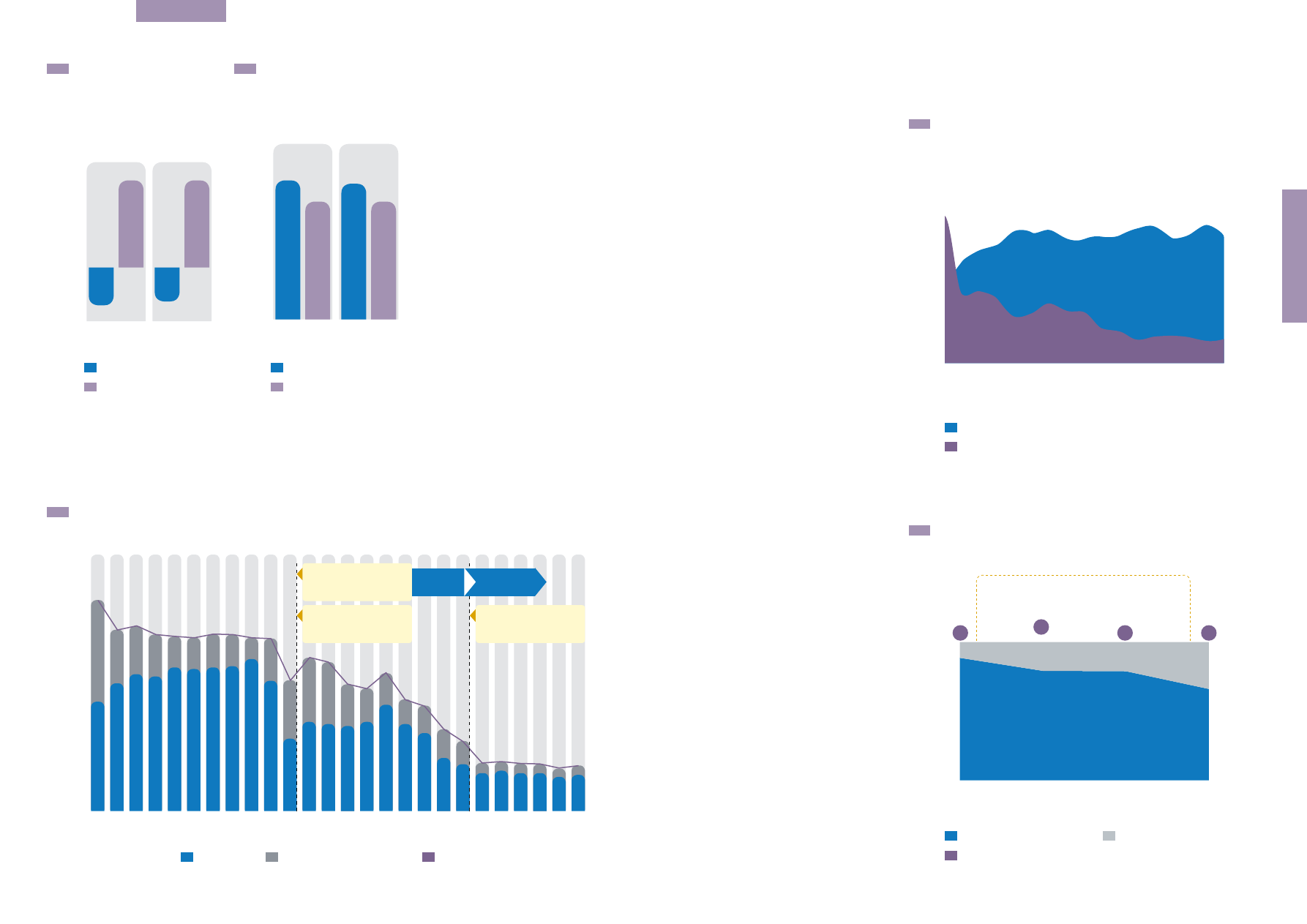

million t/year

90�0

80�0

70�0

60�0

50�0

40�0

30�0

20�0

10�0

0�0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Transit Domestic transportation Total

The Baltic pipeline route-1

started 12 MT/y

The Baltic pipeline route-2

started 25 MT/y

Bypassing pipeline to

Novorossiysk started

28 MT/y

78�0

66�9 68�5

65�3 64�6

65�4

64�0

48�0

54�9

44�9

40�9

29�8

17�2

16�9

15�2

64�1

65�2

63�6

56�7

46�7

50�9

38�5

25�2

17�6

16�8

16�0

36�9

19�2 17�9

15�2 11�2

12�0

7�6

20�6

22�4

11�7

8�1

9�7

2�7

1�8

1�4

11�2

11�3

15�0

23�5

15�3

11�1

9�4

7�4

2�0

1�6

2�1

41�1

47�7

50�6 50�1 53�4

53�4

56�4

27�4

32�5

33�2

32�8

20�1

14�5

15�0

13�8

52�9

53�9

48�6

33�2

31�4

39�8

29�1

17�8

15�6

15�2

13�9

2004-42

MT/y

2015-55

MT/y

The volume of crude oil transportation

Key problems:

1. Russia and Kazakhstan

redirected oil export routes

to Russian port terminals

Russia is working to remove

transit intermediaries as part

of the Kremlin’s geo-economic

strategy. This is precisely why

Ukraine has been facing dramatic

reductions in oil transit during

the past few years.

With the aim of bypassing

transit countries, Russia

completed construction of

the Baltic Pipeline System

(BTS-1 and BTS-2) with a

total transfer capacity of 80

million tons of oil per year.

As a result, in 2016 and 2017,

about 80% of Russia’s crude

oil and condensate exports

were seaborne. However,

regardless of the ultimate mode

of transport, most of Russia’s

crude oil exports must traverse

Transneft’s pipeline system (RF

oil pipeline operator), either

as a direct route to reach

bordering country or to reach

Russian ports. Despite the

growing share of oil supplies

from the Russian Federation

to the European market, the

transit flow via the Ukrainian

string of Druzhba oil pipeline is

dropping.

As a result of the low

diversification of transit flows,

the aggressive policies of

neighboring countries and the

slow response to changes in the

market situation, Ukraine has lost

more than 30 million tons of oil

transit flow per year since 2001.

2. Lack of diversification

Ukrainian transit oil flow

comprises only oil from Russian

producers. Transit volume

Russia and Kazakhstan redirected oil export routes to Russian

ports’ terminals since 2001

%

%

35

30

25

20

15

10

5

0

60

50

40

30

20

10

0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Share of Russia oil in EU import (left scale)

Share of Ukrainian route in Russia export (right scale)

CAGR 3�4%

CAGR –7�1%

Diversification of Hungarian import

%

120

100

80

60

40

20

0

50

45

40

35

30

25

20

15

10

5

0

2014

2015

2016

2017

% Russian Federation oil

% other oil (left scale)

Total imported volume million barrels/year (right scale)

89%

79%

79%

60%

43�7

estimated losses of Ukrainian route 2�8 million t

45�1

43�8

43�8