содержание .. 3 4 5 6 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2017 рік) - 5

OUR PERFORMANCE

ANNUAL REPORT 2017

69

68

*

high level of payments for actual consumption

NAFTOGAZ

TO SUPPLY GAS WITH DISCOUNT

CMU

OBLIGED

TO RSCs

HOUSEHOLDS*

INDUSTRIAL SECTOR

FOR CASH

NONE

PAYS NAFTOGAZ

GOR GAS

CAN BE SOLD TO THE

ATTRIBUTE GAS TO

The debt remains with RSCs

RSC is a dummy without assets

Gas is attributed to non-existing users as

their debt to RSC

SURPLUS

profit from

difference

in prices

Main

scheme

of RSC

PRICE LIMITATION ISSUES – PRICES ESTABLISHED UNDER THE PSO ARE LOWER

THAN IN THE UKRAINIAN WHOLESALE MARKET

1. Losses for the state. The under-receipt of income in comparison with the alternative to sell gas at

market prices. In turn, lower company income means lower state budget income. Even the increase

in expenses for subsidies does not change this simple rule, since by no means all consumers receive

subsidies.

2. Social injustice. The underpricing of gas sales to household consumers below the market level which

actually means hidden subsidies for gas consumers received even by those who are able to pay the

market price. Moreover, the higher the consumption – the more hidden the subsidy. Those who do not

consume gas, do not receive such subsidies at all. Such allocations of public wealth is unjust.

3. Distortion of economic incentives for energy efficiency and energy saving

4. It is impossible to create a real retail gas market. There are no substitutes to free pricing as the key

factor of market development. There is no competition without market pricing. World practice proves

that competitive pricing is better than state regulation of prices for consumers in the medium and long-

term perspective.

5. Drop in the investment attractiveness of gas production in Ukraine. Even now, private production

in Ukraine covers all consumers with an acceptable credit risk level. Therefore, investors understand that

additional volumes of produced gas would have to be sold to household consumers and heat producing

companies. Investors cannot forecast the prices to be established by the state for this category of

consumers. The impossibility of forecasting prices reduces the industry's investment attractiveness.

6. Incentives for arbitration (resale) and corruption, due to different prices for one and the same

product.

7. Difficulties in relations with international creditors, receiving respective financing and attracting

cheap loans.

problems with poor payment

discipline of regional supply

companies. As mentioned

above, during 2016-2017 trade

accounts receivable for gas sold

to regional supply companies for

resale to households increased

by USD 1 billion.

Low ROIC

33

of the “Gas production,

import and sales to RSC's for

resale to households” segment

was also low on average 4.7%

for 2016-2017 – both because

of lower than market gas

selling prices (imposed by PSO

Regulation) and accumulation of

debts.

In 2018, Naftogaz group asked

the Cabinet of Ministers of

Ukraine to compensate the loss

of UAH 111 billion for supply

of gas under public service

obligations (PSO). The right

of companies to demand the

determination of sources of

financing and the procedure for

compensation for PSO by the

government is confirmed in court.

According to the Gas Market

Law, the group has the right to

receive compensation for its

33

ROIC is calculated as NOPLAT divided by market

value of invested capital, which was determined

as a sum of invested capital in fixed assets

based on estimation of its market value and

net working capital as of the end of the year.

Market value of invested capital in fixed assets,

mostly represented by upstream assets,

was estimated as monetary value of 2P gas

reserves audited and appraised by independent

O&G consulting firm.

economically justified expenses

reduced by the income received

in the course of PSO performance,

and taking into account the

acceptable rate or return.

If PSO compensation claimed by

the company for gas sales to RSC

for resale to households was paid

for 2016 and 2017, hypothetical

ROIC of this business would be

10.1% and 14.5% respectively.

This hypothetical ROIC would be

significantly higher if compared

with unadjusted value, but it is

still lower than cost of capital of

18.7%

34

due to high invested

capital in fixed assets (mostly

34

Cost of capital is estimated by independent

appraisers to determine the fair value of

property, plant and equipment of PJSC “National

Joint Stock Company ’Naftogaz of Ukraine’” as of

31.12.2017.

production assets evaluated

according to the market value)

and net working capital.

The consideration underlying

Naftogaz group's corporate

strategy implies that an efficient

alternative to the current system

of gas supply to households is

the creation of a transparent

gas market for the population

with the possibility of selection

of the supplier. This would allow

Naftogaz group to receive the

money for the produced gas and

monetize the profit of the gas

business. So far, the gas business

is funded at the expense of

transit.

In order to do that, it is necessary

to get rid of the monopoly

intermediaries represented by

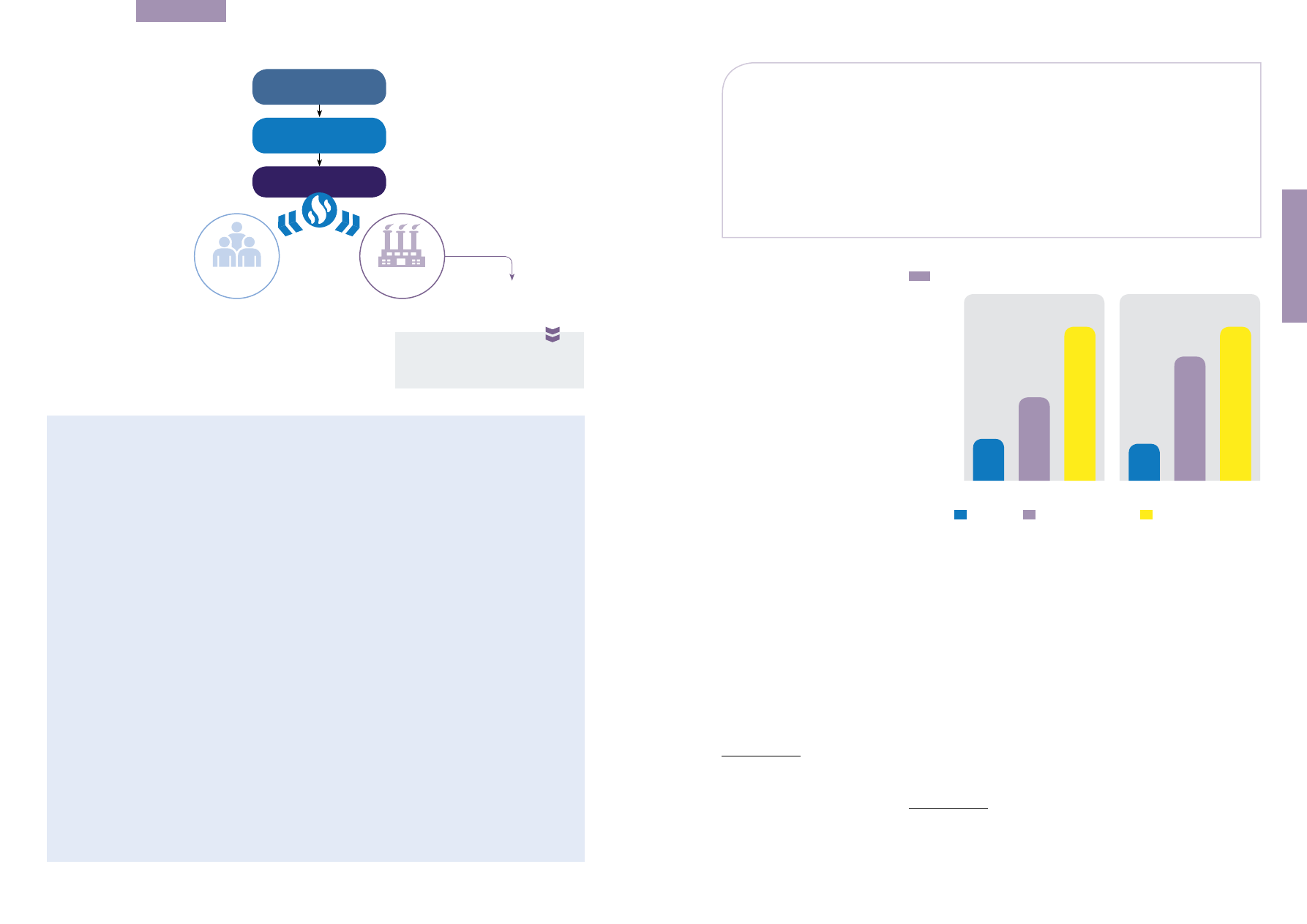

3.1%

AVERAGE OPERATING CASH FLOW MARGIN OF

"Gas production, import and sales to RSCs for resale

to households" for 2016-2017

4.7%

AVERAGE ROIC OF

"Gas production, import and sales to RSCs for resale

to households" for 2016-2017

2017

20

15

10

5

0

%

2016

ROIC Hypothetical ROIC Cost of capital rate

ROIC vs cost of capital, UAH-denominated, %

5�0

10�1

18�7

18�7

14�5

4�5