содержание .. 2 3 4 5 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2017 рік) - 4

OUR MARKET AND REFORMS

ANNUAL REPORT 2017

53

52

Main disadvantages of the existing PSO

1. The sale of gas at below

market prices and the

absence of cost-recovery

mechanisms

Prices set by the government

are lower than market prices,

so independent suppliers have

no commercial interest for the

segment. The existing PSO

includes no effective mechanisms

for enforcement of financial

settlements between market

players. Current procedures do

not allow Naftogaz to restrict gas

supply to gas retail companies

in response to non-payment.

As a result, regional gas retail

companies have accumulated

more than UAH 34 billion in debts

in the approximately 2.5 years of

their existence.

In addition, the government has

not established compensation

mechanisms and funding sources.

According to Naftogaz group΄s

assessment, the compensation

accrued to the group for the

fulfillment of the duties in the

period from 1 October 2015 to

31 December 2017, is more than

UAH 111 billion, and the company

is forced to defend its legitimate

interests in court in order to

receive compensation. The

court ordered the government

to determine the sources of

funding, and the procedure

for compensation for PSO.

However, the decision is still to be

implemented.

2. The sale of gas through

intermediaries significantly

complicates monitoring the

use of gas as intended and

ensuring payments

The lack of effective mechanisms,

which enable monitoring the use

of gas as intended, creates a basis

for abuse. Not only vulnerable

consumers benefit from PSO,

but also people with a sufficient

income to pay for gas and heat

from their own pocket, which

leads to inefficient use of the state

budget funds.

To date, there is no effective

mechanism for confirmation by

regional gas retail companies of

supply of certain volumes of gas

to specific consumers under the

special duties framework. There

is no evidence that all the gas

at a reduced price is supplied to

households. Naftogaz is interested

in identifying evidence of the

actual volumes of gas supplies

provided to households because

it is the basis for calculating

Naftogaz group΄s expenses for

fulfilling its special duties. In

the absence of compensation

for the performance of special

duties, these costs become

Naftogaz group΄s losses.

2015–2017 PSO-RELATED LOSSES

COMPENSATION STATUS

111

UAH bn

74.8

UAH bn

24.1

UAH bn

12.1

UAH bn

incl.

• UGV and Naftogaz

are entitled to a compensation

of losses

related to PSO according to the law On Natural Gas Market

• CMU

failed to determine the compensation policy

when

imposing the PSO in 2015 and 2017

• Naftogaz was successful in court and court of appeal in proving

CMU

has to determine the policy and funding sources

Compensation for losses

related to PSO claimed by

UGV and Naftogaz

UGV

Foregone

revenue

Naftogaz

Related

losses

Naftogaz

Related bad

debt reserve

Gas supply and retail to households in PSO

Problem # 1.

Lack of transparency and access

to the consumer data base

Naftogaz, as a natural gas

supplier to households,

is exposed to many risks:

fluctuations in prices, volumes

and exchange rates, as well as

gas storage costs. Oblgazzbuts as

intermediaries only bill end users.

At the same time, they do not

provide Naftogaz with data on

actual volumes of gas usage. The

consumers do not pay directly

to Naftogaz, but to the accounts

of oblgazzbuts. As of 1 June

2017, Naftogaz has lost access to

data on actual gas payments by

customers.

Problem # 2.

Collecting debts

Naftogaz has no data on

debtors and so cannot

collect debts from them.

This is a function of the

regional retail companies and

subject to inefficiency. Since

oblgazzbuts do not bear the

financial costs of servicing the

gas debt to Naftogaz, they

have no effective incentive

to work efficiently with

debtors, which leads to the

accumulation of gas debts.

Problem # 3.

Consumption data

manipulation

An internal audit of

Kirovohradgaz, after the

restoration of operational

control and change of

management in June 2017,

revealed more than 9.8 mcm of

gas allocated to non-existing

consumers or so-called "dead

souls". Kirovohradgaz reported

to law enforcement authorities

about the detected facts,

but similar cases may exist in

other gas distribution system

operators (“oblgazes”) and

oblgazzbuts, which causes

losses to Naftogaz.

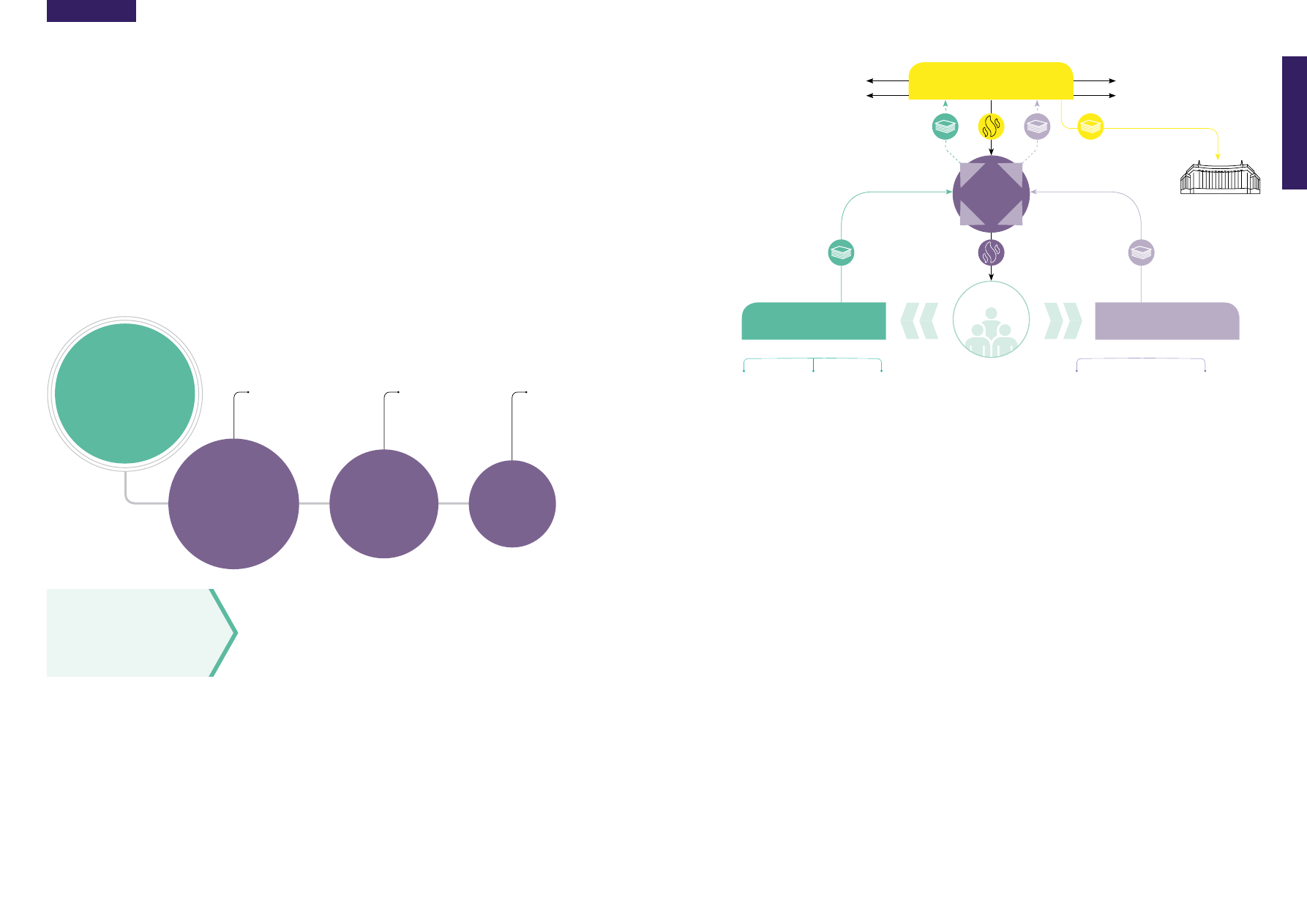

OBLGAZZBUTS

NAFTOGAZ

PRICE RISK

FINANCE AND GAS STORAGE COST

CURRENCY RISK

VOLUME RISK

Taxes and dividends

HOUSEHOLDS

Consumed

and paid

Consumed,

covered by gov't

Consumed

and not paid

Not consumed,

below norms

Not consumed,

fake addresses

PROBLEM

1

Naftogaz doesn't

get due share of

paid amounts

PROBLEM

2

Inefficient debt

collection

PROBLEM

3

Gas sold to ineligible

consumers, Naftogaz

will never be paid

PROBLEM

4

Risk of Naftogaz not

getting due share of

paid amounts

PROBLEM

5

Gas sold to ineligible

consumers,

government overpays

PAYABLE BY SUBSIDIES

PAYABLE BY CASH