содержание .. 1 2 3 4 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2017 рік) - 3

OUR MARKET AND REFORMS

ANNUAL REPORT 2017

37

36

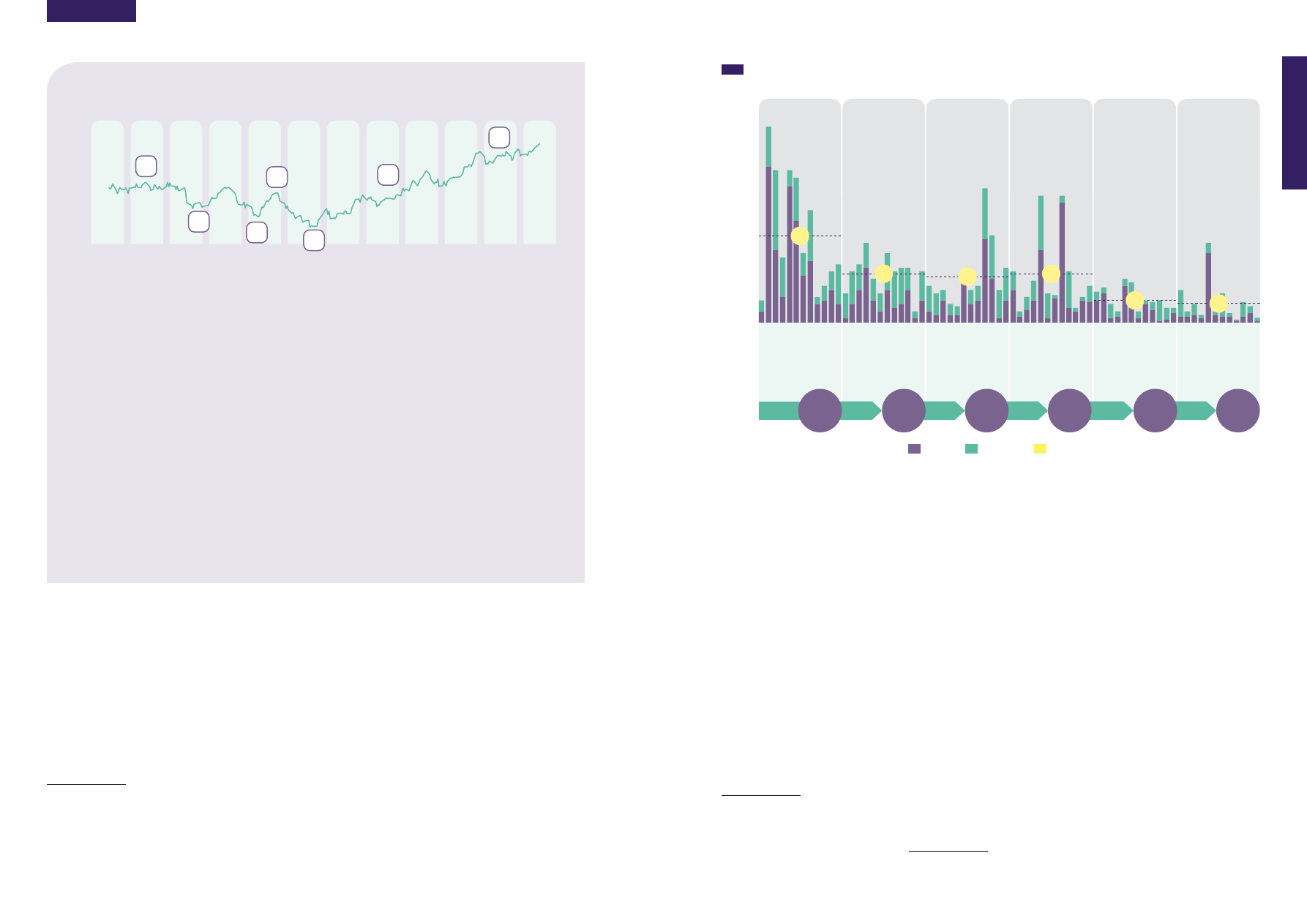

At the same time, 2017

demonstrated a record low

capacity of new discovered

oil reserves, with the average

capacity of about 550 million

barrels of oil equivalent per

month

19

. Most alarming is

the fact that the reserve

replacement ratio

20

(for oil and

gas) reached only 11% in 2017

compared to more than 50%

19

Rystad Energy https://www.rystadenergy.

com/newsevents/news/press-releases/

all-time-low-discovered-resources-2017/

20

The reserve replacement ratio is the ration

of the number of reserves discovered during

the year to the global hydrocarbon production

during the year.

in 2012. Such a low reserve

replacement level can have a

negative impact on the supply

side over the next decade,

which will accordingly affect

world energy prices.

Overall, a steady trend towards

rising prices on the oil market

was observed in 2017, which

is primarily due to the freezing

of oil production volumes

by OPEC countries. The

current high oil prices make

investments in oil production

more attractive, including in

Ukraine. However, since Ukraine

is a net importer of oil and

oil refining products, Ukraine

is forced to spend additional

currency resources for their

purchase. For instance, in 2017

alone, the total expenditures

of the country on oil and

petroleum product imports

increased by 33%. In case of

further growth of the world oil

prices and without building up

domestic production of oil and

petroleum products in Ukraine,

this trend will negatively affect

the balance of payments of

the country and can lead to a

reduction in GDP.

Major events that impacted the price situation on the oil market in 2017

70

65

60

55

50

45

40

January

February

March

April

May

June

July

August September October November December

1

2

3

4

5

6

7

1. For most of the first quarter of 2017, prices were stable against the background of the agreement reached by

OPEC member countries at the end of 2016 on "freezing" the level of oil production.

2. Prices began to decline in March 2017 after the publication of several consecutive reports of the US Energy

Information Administration on increases in the US commercial reserves of oil.

3. As a result of the shutdown of a number of major refineries in the United States and other parts of the world for

maintenance, another fall in prices occurred in May 2017 and buildup of commercial crude oil reserves in the

United States.

4. In June 2017, prices began to increase based on the expectations of market participants for further reduction of oil

production by OPEC member countries in order to balance the market.

5. The market response to the OPEC decision to maintain oil production at the current level was a rapid drop in

prices in July 2017.

6. Since the beginning of the third quarter of 2017, there has been evidence that proved the effectiveness of

the OPEC member states agreement on the oil output cut. In addition, a high level of loading of refineries and

demand for refined products was observed. The level of loading of European refineries grew from 89% in Q2 2017

to 92% in Q3 2017; overall the global oil increase in Q3 was 1.1%.

7. In November 2017, OPEC member states at their regular meeting decided to extend the decision to restrict oil

production until the end of 2018.

European market for oil and petroleum products

2017 can be considered a success

for European refineries. Due to

the oil refining margin, which was

higher than in 2016, the European

refineries utilization rate was

stable during 2017

21

.

European oil refining capacities

dropped by 15% between 2010

and 2017 (from 865 million t/ year

to 740 million t/year)

22

and in

2017 they comprised about 14%

of global capacity. In view of

world trends, further reduction in

production capacities is possible

in the period to 2025 due to:

– an increase in petroleum

products and construction

21

Monthly OPEC Report (2017), IEA Global Margin

Conversion Indicator

22

International Refining and Petrochemical

Conference (IRPC) in Europe in 2017 (from the

speech of Manfred Litner, member of executive

board of OMV AG)

of new oil refineries on other

continents

23

;

– an increase in the share of

imports of finished petroleum

products in Europe against the

background of reduction of

emission quotas for harmful

substances.

One of the factors that positively

impacted the operations of the

European refineries was the

decrease in production and in

excess supply on the market after

the 2017 agreement between

the OPEC member states was

reached. This factor operates

in a way that the reduction of

production was mainly due to

heavy grades of oil, which are

usually processed by refineries

with a high level of complexity

23

Global Data

and located outside of Europe.

The European oil refineries

process lightweight petroleum,

which is logistically available for

delivery (oil from Kazakhstan,

Azerbaijan, Libya and Nigeria

is not within the scope of

petroleum output cut agreed by

the OPEC member countries).

In Q3 and Q4 2017, the

petroleum products price

trend in Europe was much

slower than the global oil price

trend. For instance, the oil

price growth during August-

December 2017 amounted to

about 30% (from 49 to 64 USD/

barrel), while the petroleum

products price growth in

European countries amounted

to about 10% for gasoline and

diesel fuel, which impacted the

oil refining margin curve for

European refineries.

Gas Liquids Year average

Global conventional discoveries, billion boe

6

5

4

3

2

1

0

January

April

July

Oct

ober

January

April

July

Oct

ober

January

April

July

Oct

ober

January

April

July

Oct

ober

January

April

July

Oct

ober

January

April

July

Oct

ober

2012

2013

2015

2014

2016

2017

TOTAL VOLUME

PER YEAR

30

16

15

15

8

6�7

2�5

1�3

1�3

0�6

0�6

1�3