содержание .. 2 3 4 5 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2018 рік) - 4

55

54

2018

OPERATIONS

ANNUAL REPORT 2018

INTEGRATED GAS

BUSINESS DELIVERY UNIT

Integrated Gas Business Delivery Unit structure

Integrated Gas Business Delivery Unit

(further – Integrated Gas or Integrated

Gas BDU) includes all activities of

Naftogaz group related to exploration

and production of domestic natural gas

and liquid hydrocarbons, imports, sales,

trading, supply and distribution activities

of Naftogaz group.

The Integrated Gas BDU composition

aims to enable end-to-end P&L

responsibility for gas-related activities –

from producing or importing a molecule

of hydrocarbons to getting it to the final

customer of Naftogaz group. Integrated

Gas primarily focuses on the following

sets of activities along the gas value

chain:

1) in upstream, Integrated Gas focuses

on growth and commercialization

of the hydrocarbons reserve base

of Naftogaz group through effective

management of its brownfield

and greenfield license portfolio,

improving its own geological and

reservoir management capabilities

and exploring partnership options

for de-risking and accelerating

reserve development;

2) in midstream, Integrated Gas focuses

on working efficiently with the

transmission & storage business of

Naftogaz group to ensure security

of supply while optimizing capital

investment into natural gas stocks;

3) in downstream, Integrated Gas focuses

on developing trading capability while

building out its retail function and

working on its accounts receivable

portfolio.

HYDROCARBON RESERVES AND RESOURCES OF NAFTOGAZ GROUP

Natural gas, bcm Oil and gas

condensate, mmt

Natural gas (mmboe)*

Oil and gas

condensate

(mmbbls)*

Naftogaz**

proven developed

-

-

-

-

proven undeveloped

-

-

-

-

probable

-

-

-

-

production of hydrocarbons

-

-

-

-

increase in hydrocarbons reserves

-

-

-

-

Reserves as of 31.12.2018

-

-

-

-

Resources as of 01.01.2018

34.96

1.31

209.73

9.52

resources located in the Joint Forces Operation (JFO) zone and the

annexed territory

34.96

1.31

209.73

9.52

Resources as of 01.01.2016 (excluding the JFO zone and the annexed

territory)

-

-

-

-

Ukrgasvydobuvannya

proven developed

201.73

4.03

1 210.37

36.40

proven undeveloped

17.34

1.09

104.06

10.27

probable

28.87

1.49

173.19

11.53

production from 1.07.2017 till 31.12.2018 (2)

23.27

0.68

139.62

5.94

increase in hydrocarbons reserves in 2017 and 2018 (1)

31.63

1.96

189.76

14.25

Reserves as of 31.12.2018

256.29

7.9

1 537.16

66.51

Resources as of 30.06.2018 (3)

25.84

155.06

Ukrnafta

proven developed

14.52

14.48

87.10

105.42

proven undeveloped

7.50

9.66

45.00

72.96

probable

10.72

16.28

64.34

121.37

production from 01.07.2016 till 31.12.2018 (2)

2.84

3.58

17.01

21.49

increase in hydrocarbons reserves from 01.07.2016 till 31.12.2018

-

-

-

-

Reserves as of 31.12.2018

29.90

36.83

179.43

278.25

Resources as of 01.01.2018 (4)

17.12

20.63

102.74

150.19

Egypt

proven developed (5)

0.27

0.40

1.65

2.91

proven undeveloped (5)

0.12

0.14

0.73

1.06

probable

0.06

0.16

0.39

1.17

production of hydrocarbons from 1.04.18 till 31.12.18 (2)

0.03

0.07

0.15

0.52

increase in hydrocarbons reserves

-

-

-

-

Reserves as of 31.12.2018

0.44

0.63

2.62

4.62

Resources as of 01.01.2018

0.37

1.15

2.20

8.42

Group

proven developed

216.52

18.91

1 299.12

144.72

proven undeveloped

24.97

10.89

149.79

84.29

probable

39.65

17.93

237.92

134.06

production of hydrocarbons (2)

26.13

4.33

156.78

27.95

increase in hydrocarbons reserves (2)

31.63

1.96

189.76

14.25

Reserves as of 31.12.2018

286.63

45.36

1719.21

349.38

Resources as of 31.12.2018

43.33

21.78

256.41

158.55

Sources:

The audit of hydrocarbon reserves of Ukrgasvydobuvannya performed by Miller and Lents as of 30 June 2017. The audit of reserves, revenue and resources in some deposits of Ukrnafta

performed by DeGolyer and MacNaughton as of 1 July 2016. The audit of hydrocarbon reserves of Naftogaz group in the Arab Republic of Egypt and additional report on assessment of

contingent and prospective resources performed by Ryder Scott as of 30 April 2018. The audit of the group’s reserves with assessment of prospective resources of Naftogaz of Ukraine

performed by Ryder Scott as of 31 December 2014.

* To convert the volumes of oil and gas condensate into barrels, ratios according to the audit and their physical properties were used: for oil deposits in the ARE, a ratio of

7.33 bbl/t was used; for light liquid hydrocarbons (mostly condensate) of the deposits of Ukragazvydobuvannya, the ratio varies from 7.75 to 9.4 bbl/t (average 8.8 bbl/t); for

Ukrnafta, the ratios vary from 7.22 to 7.42 bbl/t for oil and from 8.07 to 8.61 bbl/t for condensate; in the event of lack of updated audited ratios, a ratio of 7.28 bbl/t was used.

To convert volumes of natural gas into oil equivalent, a ratio of 1 boe = 167 cubic m was used.

** In 2017, State Geological and Subsurface Survey of Ukraine (SGSSU) annulled special permits for the use of subsoil and Naftogaz’s right explorated within the Budyschan-

sko-Chutivsky, Obolonsky and Pysarivsky permits, and licensed fields located in the ATO zone and Black Sea and Azov Sea areas were expropriated, therefore Naftogaz’s

resources of hydrocarbons as of 31 December 2018 are zero.

(1) - an increase in hydrocarbon reserves of Ukrgasvydobuvannya is not audited under SPE PRMS and is the company’s estimate in accordance with the Ukrainian classification

(audits are expected in May-June 2019);

(2) - cumulative production data of Ukrgasvydobuvannya since the last audit of reserves and resources till 31 December 2018 are presented;

(3) – volumes of liquid hydrocarbons of perspective resources of Ukrgasvydobuvannya were converted into gas volume equivalent using a constant ratio of 6 mcf/boe

(4) – Contingent resources resources of Ukrnafta (Contingent resources) with uncertain probability of commercialization, and the application of risk factors does not equalize this

probability with the class of recoverable reserves;

(5) – proved volumes of commercial extractable hydrocarbon reserves in the ARE include volumes of hydrocarbons classified as contingent resources (2C Contingent resources,

under SPE PRMS) due to the lack of a full-scale field development project approved by the shareholders.

Integrated Gas Business Delivery Unit structure

Gas production, import and sales to

RSC’s for resale to households

and direct supply to households

Gas production, imports and supply

to MHEs for the needs of households

Gas production, imports and supply

to other customers under PSO

Gas imports and supply

to other customers outside PSO

Oil and condensate production

Naftogaz

Teplo

Exploration

Production

Imports

Transmission

Storage

Gas

wholesale

Distribution

Supply

Ukrgasvydobuvannya

Ukrgasvydobuvannya

Naftogaz

of Ukraine

Naftogaz

Trading

Europe

Naftogaz

Trading

Naftogaz

of Ukraine

Kirovogradgaz

GSC

Naftogaz of Ukraine

Integrated Gas Business Delivery Unit

Not applicable

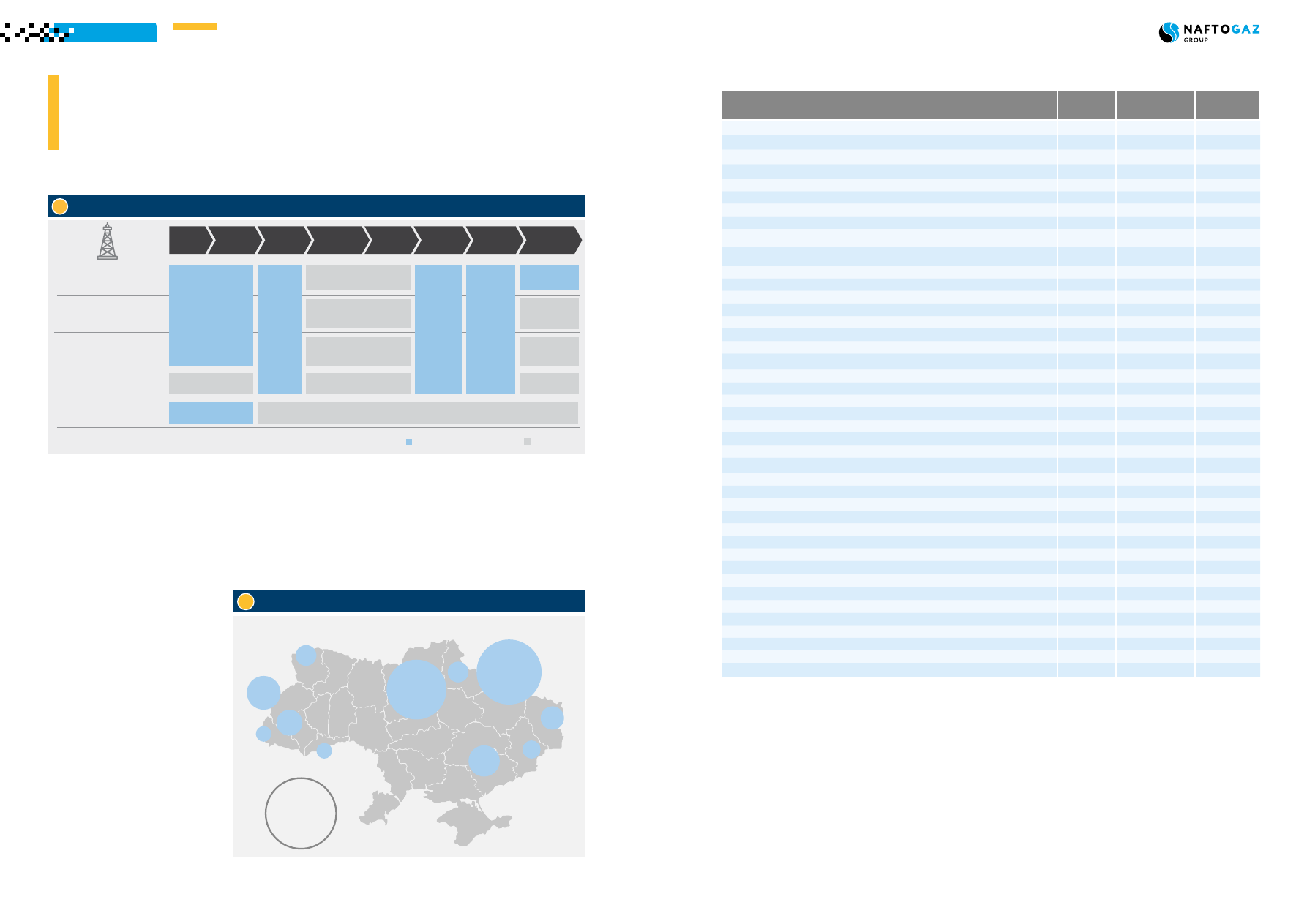

The geographical breakdown of natural gas production by UGV in 2018, mcm

Total

15 497

mcm

KHARKIV

DNIPROPETROVSK

POLTAVA

LUHANSK

DONETSK

SUMY

CHERNIVTSI

VOLYN

LVIV

IVANO-FRANKIVSK

ZAKARPATTYA

8 003

6 261

431

144

554

50

21

29

1

2

0,6

Source: Ukrgasvydobuvannya