содержание .. 13 14 15 16 ..

НАК „НАФТОГАЗ УКРАЇНИ“. Річний звіт англійською (2017 рік) - 15

FINANCIAL STATEMENTS

ANNUAL REPORT 2017

229

228

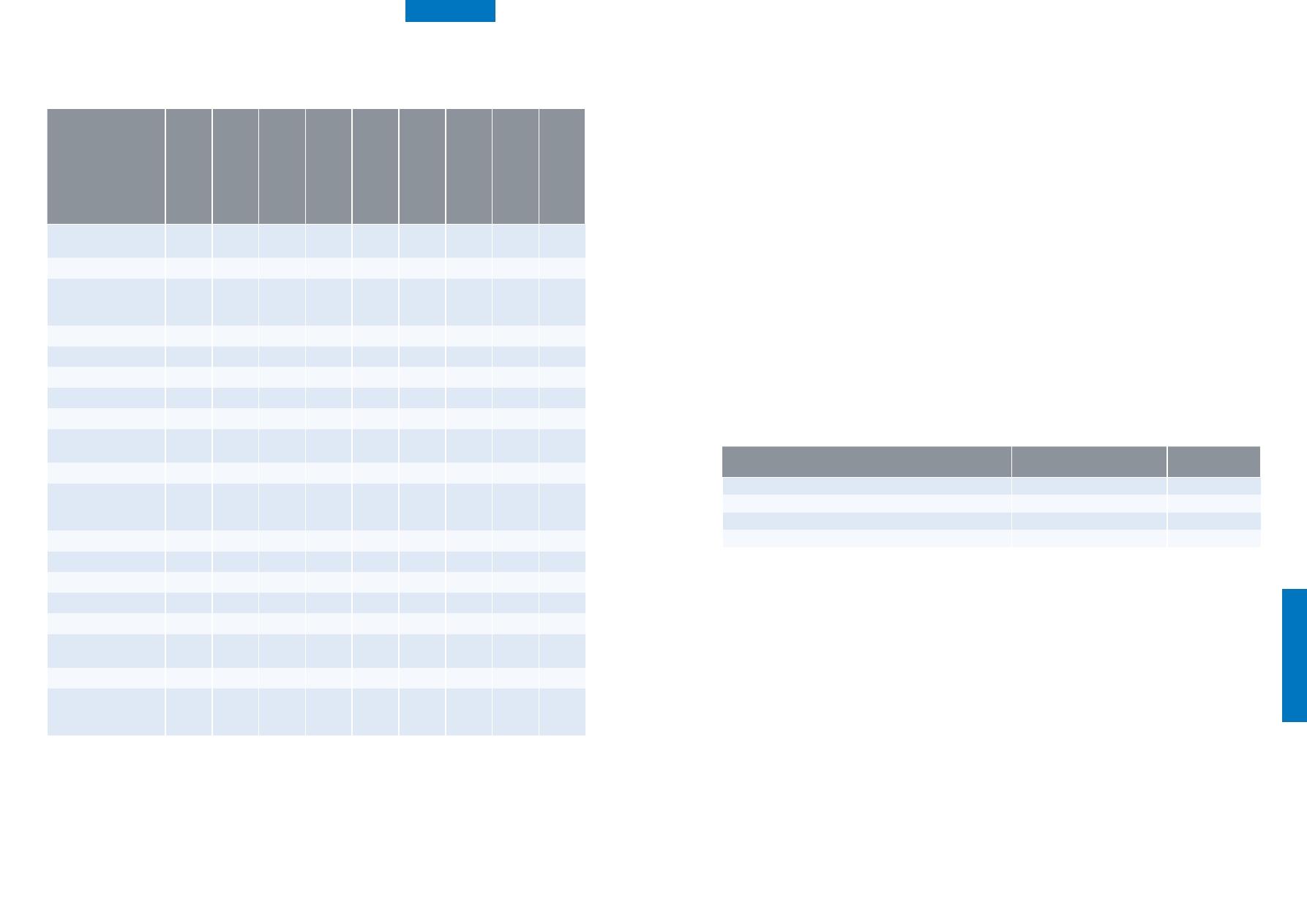

6� PROPERTY, PLANT AND EQUIPMENT

Movements in the carrying amount of property, plant and equipment were as follows:

In millions of Ukrainian

hryvnias

Pipelines and r

ela

ted

equipmen

t

O

il and gas pr

oducing

pr

oper

ties

M

achiner

y and

equipmen

t

Buildings

Cushion gas

D

rilling and e

xplor

ation

equipmen

t

O

ther fix

ed assets

Construc

-tion in

pr

og

ress

Total

Net book value at

31 December 2015

210,782

53,405

75,920

62,392 142,140

582

3,900

10,675 559,796

Cost or valuation

212,066

53,826

76,593

63,439 142,140

861

5,122

11,617 565,664

Accumulated

depreciation and

impairment

(1,283)

(420)

(673)

(1,047)

–

(279)

(1,224)

(942)

(5,868)

Additions and transfers

(12,549)

5,487

38,019 (22,236)

–

790

(2,588)

1,851

8,774

Revaluation

–

–

–

–

13,282

–

–

–

13,282

Disposals

(3)

(33)

(16)

(68)

–

(34)

(1)

(247)

(402)

Depreciation charge

(7,137)

(5,719)

(7,104)

(3,521)

–

(295)

(307)

– (24,083)

Impairment

(20)

(799)

(1)

(2,156)

(1,856)

(91)

–

(783)

(5,706)

Net book value at

31 December 2016

191,074

52,342 106,818

34,411 153,566

952

1,002

11,496 551,661

Cost or valuation

199,270

59,300 116,533

39,194 155,422

1,447

2,724

13,117 587,007

Accumulated

depreciation and

impairment

(8,196)

(6,958)

(9,715)

(4,783)

(1,856)

(495)

(1,722)

(1,621) (35,346)

Additions and transfers

(522)

4,335

2,106

1,673

–

870

338

6,740

15,540

Revaluation

(42,181)

27,140

(8,506)

(6,383)

(3 526)

548

(99)

– (33,007)

Disposals

–

(19)

(20)

(6)

–

(20)

(4)

(289)

(358)

Depreciation charge

(16,882)

(6,202) (14,919)

(2,728)

–

(565)

(292)

– (41,588)

Impairment

–

–

(41)

(119)

–

(74)

(6)

(526)

(766)

Net book value at

31 December 2017

131,489

77,596

85,438

26,848 150,040

1,711

939

17,421 491,482

Cost or valuation

132,909

77,944

86,105

27,484 150,045

1,738

2,128

19,443 497,796

Accumulated

depreciation and

impairment

(1,420)

(348)

(667)

(636)

(5)

(27)

(1,189)

(2,022)

(6,314)

The Group engaged

independent appraisers to

determine the fair value of

its major groups of property,

plant and equipment as at

31 December 2017. The fair value

was determined in accordance

with International Valuation

Standards.

Taking into account the nature

of the Group’s property, plant

and equipment, fair value was

determined using depreciated

replacement cost for specialised

assets, and using market-based

evidence for non-specialised

assets. Consequently, the

fair value of main producing

properties and equipment was

primarily determined using

depreciated replacement cost.

This method considers the cost

to reproduce or replace the

property, plant and equipment,

adjusted for physical, functional

and economic depreciation, and

obsolescence. The depreciated

replacement cost was estimated

based on internal sources and

analysis of available market

information for similar property,

plant and equipment (published

information, catalogues,

statistical data etc), and industry

experts and suppliers.

The results obtained using

different valuation approaches

provided evidence of the

existence of economic

obsolescence and impairment

costs. Economic obsolescence

is caused by the fact that

replacement cost of assets less

physical depreciation exceeded

the future economic benefits

that could be obtained from

the use of assets (with future

economic benefits calculated

based on current estimates

of the Group’s management,

expectations of independent

appraisers and consensus

forecasts). Therefore, the fair

value of specialised assets

was determined using the

depreciated replacement

cost approach as adjusted

for economic obsolescence

amount. If the fair value is lower

than carrying value of property,

plant and equipment, an

impairment loss is recognised

(Note 26).

The major part of economic

obsolescence identified

is attributed to the cash

generating unit “Gas

Transmission System”. It is

explained by the implied

expectation of the Group’s

management that there would

not be any gas transit flows

starting from 1 January 2020

after the expiration of existing

Gas Transit Contract with

Gazprom, because currently

Gazprom has not booked any

gas transit capacities beyond

2019 and is actively investing in

construction of alternative gas

pipelines bypassing Ukraine.

Should the assumption of no

transit flows from 1 January

2020 change, this could have

resulted in lower economic

obsolescence per results of

income approach in valuation

procedures.

The following table summarises

values of property, plant and

equipment by selected cash

generating units based on

different valuation approaches as

at 31 December 2017:

Cash generating unit

In millions of Ukrainian hryvnias

Cost Approach (net replacement

costs less physical depreciation)

Income Approach

Gas Transmission System

419,309

188,628

Underground Gas Storages

160,533

126,579

Gas upstream, refinery and fuel filing stations

120,479

91,094

Oil transmission and transit

15,923

14,444

Group’s management

expectations of gas transit

flows after 1 January 2020

(Note 27) is the main

assumption that affected both

revaluation of property, plant

and equipment and remaining

useful lives revision for gas

transit assets included to the

”Gas Transmission System” cash

generating unit. Expectation of

no gas transit flows after this

date has resulted in shortened

useful lives for gas transit assets

planned for decommissioning

after 31 December 2019, their

higher depreciation in 2017,

and lower net replacement

costs less physical depreciation

as at 31 December 2017.

Should expectation of material

transit beyond 2019 have

been used for revaluation,

net replacement costs less

physical depreciation of “Gas

Transmission System” cash

generating unit would be

10% higher. For other assets,

expectation of no gas transit

flows after 1 January 2020

has resulted in a lower value

under income approach

with respective impairment

loss, if any, according to the

accounting policy (Note 26).

In 2017, the depreciation

and depletion expenses of

UAH 39,144 million (2016:

UAH 22,387 million) was

included in cost of sales,

UAH 604 million (2016:

UAH 1,065 million) in

other operating expense,

UAH 775 million (2016:

UAH 631 million) were

capitalised in the cost of

property, plant and equipment,

and UAH 1,085 million were

capitalised in cost of inventories.

As at 31 December 2017 and

2016, the Group has pledged

its property, plant and equip-

ment with carrying amount

of UAH 2,682 million and

UAH 10,536 million, respec-

tively, to secure its borrowings

(Note 14).

Included in property, plant

and equipment in 2016

are capital expenditures of